How much does small business insurance cost in New York? Small business insurance costs $45–$220/month on average. See real 2026 rates by policy type and industry in New York, then get a free quote in minutes.

Most small businesses pay approximately $100 to $300 per month for core insurance coverage, depending on the type of business, location, payroll, revenue, claims history, and coverage limits.

A standalone general liability insurance policy may cost around $45–$65 per month for lower-risk businesses, while a Business Owner’s Policy (BOP) commonly ranges from $80–$150 per month for qualifying businesses.

New York businesses may pay higher premiums than businesses in many other states because of factors including higher property values, increased litigation exposure, payroll costs, and dense urban operating environments.

Below is a breakdown of what small businesses can expect to pay in 2026 by policy type, industry, and risk factors.

📞 Need help finding the right coverage? Call Weinsurexyz at (888) 540-7374. Our licensed insurance professionals compare options from multiple carriers for New York businesses.

Average Small Business Insurance Cost by Policy Type

| Insurance Policy | Average Monthly Cost | Average Annual Cost |

| General Liability Insurance | $45–$65 | $540–$780 |

| Business Owner’s Policy (BOP) | $80–$150 | $960–$1,800 |

| Workers’ Compensation Insurance | Varies by payroll and classification | Varies |

| Professional Liability / Errors & Omissions | $50–$85 | $600–$1,020 |

| Commercial Auto Insurance | $150–$400+ per vehicle | $1,800–$4,800+ per vehicle |

| Commercial Umbrella Insurance | Approximately $40–$125/month additional | Approximately $500–$1,500/year additional |

Insurance premiums vary significantly based on business type, location, revenue, employees, claims history, coverage limits, and carrier underwriting.

Why Small Business Insurance Costs More in New York

New York businesses often face unique insurance pricing factors compared with businesses in other parts of the country.

Common reasons include:

- Higher litigation costs — Liability claims in heavily populated areas can result in higher defense expenses and settlements.

- Higher property values — Commercial buildings, equipment, and inventory may cost more to insure.

- Workers’ compensation requirements — New York businesses must carry workers’ compensation coverage for most employees, and premiums depend heavily on payroll and job classifications.

- Urban exposure — Businesses operating in New York City and surrounding areas often face increased customer traffic, vehicle exposure, and third-party liability risks.

Working with an independent insurance broker can help businesses compare carriers that understand New York industries and regulations.

Small Business Insurance Cost in New York by Location

Insurance rates can vary significantly depending on where a business operates.

New York City

Businesses in NYC often experience higher insurance costs because of:

- Higher commercial rents and property values

- Greater customer and pedestrian exposure

- Higher claim severity

- More complex liability risks

Industries such as restaurants, contractors, retail stores, and transportation companies may see especially large differences.

Long Island

Businesses may experience higher premiums due to:

- Higher property replacement costs

- Higher payroll expenses

- Coastal weather exposure

Upstate New York

Businesses in areas such as Albany, Rochester, Buffalo, and Syracuse may have different pricing factors, including lower population density and different commercial property costs.

Your actual premium depends on your individual risk profile rather than location alone.

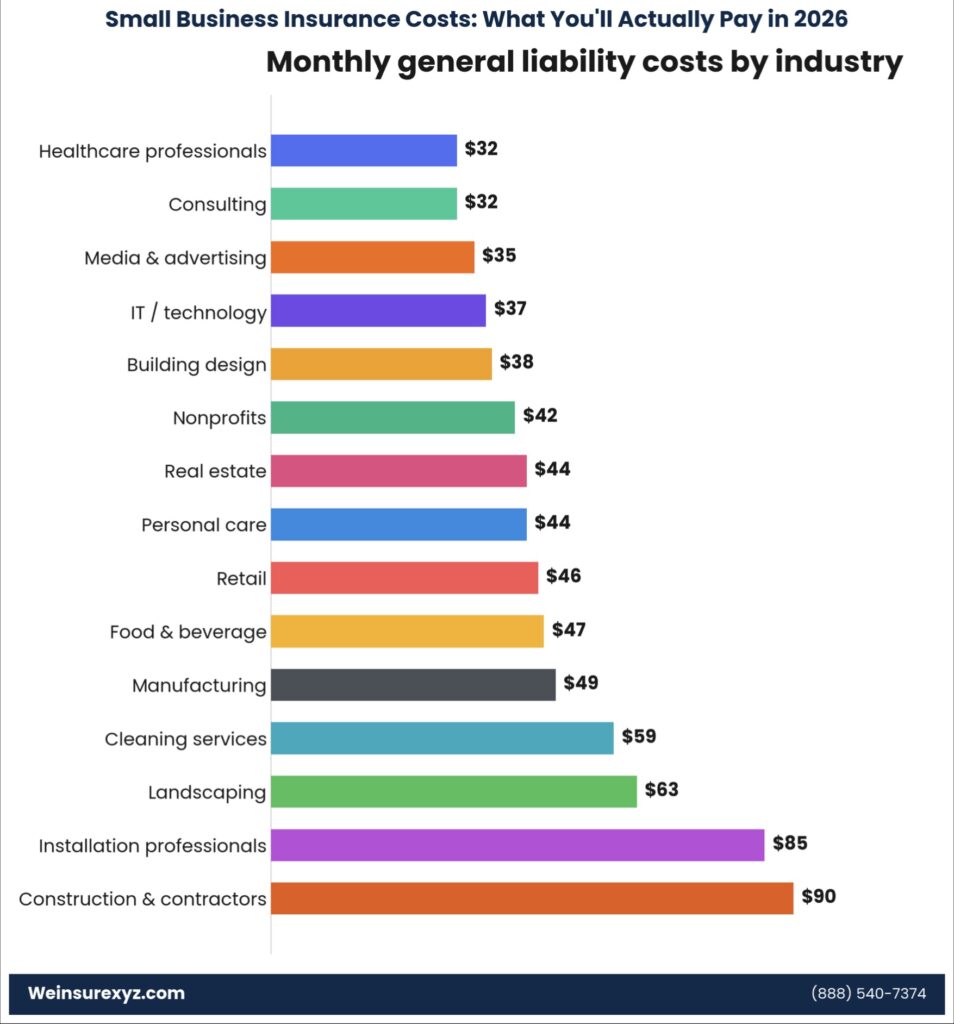

Small Business Insurance Cost by Industry

Your industry classification is one of the biggest factors affecting your insurance premium.

A consultant and a roofing contractor may both operate small businesses, but their insurance costs can be dramatically different because their risks are not the same.

| Industry | General Liability Cost Estimate | Additional Considerations |

| Consultants, accountants, IT professionals | $35–$55/month | Often require professional liability/E&O coverage |

| Restaurants and bars | $60–$150/month | Food liability, liquor exposure, and customer injuries affect pricing |

| Contractors and construction businesses | $75–$200+/month | Workers’ compensation and equipment risks increase costs |

| Trucking and transportation | $60–$120/month for liability only | Commercial auto is often the largest expense |

| Cleaning and janitorial companies | $50–$100/month | Off-site customer work increases liability exposure |

| Landscaping businesses | $75–$150/month | Equipment, vehicles, and employee injuries affect rates |

| Staffing agencies | $50–$100/month | May require EPLI and specialized coverage |

What Factors Affect Small Business Insurance Cost?

Insurance companies evaluate several factors when determining your premium:

1. Industry Classification

Your business class code is one of the most important pricing factors.

Incorrect classification can result in:

- Paying too much

- Incorrect coverage

- Problems during claims

2. Payroll and Number of Employees

Workers’ compensation premiums are largely based on payroll and employee job classifications.

More employees usually mean higher premiums.

3. Claims History

Businesses with fewer claims generally receive better pricing opportunities.

4. Coverage Limits

Higher limits provide more protection but generally increase premiums.

5. Deductible Choice

A higher deductible can reduce premiums, but businesses should choose a deductible they can comfortably afford if a claim occurs.

6. Business Experience

Established businesses with a strong insurance history may receive better underwriting consideration than brand-new operations.

How to Lower Your Small Business Insurance Cost

1. Bundle Policies Into a BOP

A Business Owner’s Policy combines general liability and commercial property coverage and may be more affordable than purchasing separate policies.

2. Compare Multiple Insurance Carriers

Insurance companies price risks differently.

An independent broker can compare multiple carriers instead of limiting you to one insurance company.

3. Review Your Classification Codes

A classification review can identify whether your business is properly categorized.

4. Improve Workplace Safety

Safety programs, employee training, and risk management practices may help reduce claims.

5. Review Coverage Annually

Your business changes over time. Annual insurance reviews help ensure you are not paying for unnecessary coverage or missing important protection.

Frequently Asked Questions

How much does small business insurance cost per month in New York?

Most small businesses in New York pay approximately $100–$300 per month for basic coverage, although contractors, restaurants, transportation companies, and businesses with employees may pay substantially more.

How much does a $1 million liability insurance policy cost for a small business?

A $1 million general liability policy is common for many small businesses. The cost depends on industry, location, revenue, claims history, and the type of work performed.

Is general liability insurance cheaper than a BOP?

Yes. General liability alone is usually less expensive. However, a BOP can provide broader protection by combining liability and property coverage and may cost less than purchasing separate policies.

Does workers’ compensation cost more in New York?

Workers’ compensation pricing depends on payroll, employee classifications, claims history, and insurance carrier rates. Higher-risk industries such as construction and transportation typically have higher workers’ compensation costs.

What is the cheapest way to get business insurance in New York?

The best way to reduce costs is usually comparing multiple carriers, selecting appropriate coverage limits, maintaining a good claims history, and ensuring your business is correctly classified.

Estimate Your Business Insurance Cost

Want a faster estimate?

Use our business insurance quote tool to compare options based on:

- Industry type

- Number of employees

- Location

- Revenue

- Coverage needs

Get a personalized estimate instead of relying only on averages.

Get Your Actual Small Business Insurance Rate

Insurance averages are only a starting point.

Your actual premium depends on your business operations, employees, location, coverage requirements, and claims history.

Weinsurexyz helps New York business owners compare commercial insurance options from multiple carriers to find coverage that fits their needs and budget.

📞 Call (888) 540-7374

Or request a free quote online.

Sources and References

Insurance pricing information is based on industry cost reports and insurance market data from sources including:

- Insurance Information Institute commercial insurance information

- New York Workers’ Compensation Board resources

- National Council on Compensation Insurance (NCCI) workers’ compensation research

Actual premiums vary by insurer and business characteristics.